פורסם: 20/10/2020, הפוסט עודכן בתאריך: 17/4/2021.

המסמך שלהלן מובא כחלק מנסיון לברר היכן עומדים הרגולטורים הישראלים המפקחים על הגופים הפיננסיים (במיוחד אלו שמפקחים על הגופים המוסדיים, קרנות הפנסיה וקופות הגמל ועל הבנקים) ביחס לרגולטורים האירופאים בנושאים הקשורים להתחממות הגלובלית ולמשבר האקלים וזאת לאחר שהרגולטורים הישראלים החלו להתייחס לנושא מול הגופים המפוקחים (בהתייחס לגופים המוסדיים ראו טיוטת תיקון חוזר "ניהול נכסי השקעה" (שיקולי השקעה הנוגעים להיבטים סביבתיים, חברתיים והיבטי ממשל תאגידי); וביחס לבנקים ראו מכתב המפקח על הבנקים לתאגידים הבנקאיים וחברות כרטיסי אשראי – הנדון: ניהול סיכונים סביבתיים).

המסמך המפורט של רשות ה-EBA מראה שהרגולטור האירופי מבין את סיכוני האקלים וכי הוא עושה מאמץ להנגיש את המידע לגופים המפוקחים.

חשוב: נייר העמדה המובא להלן הינו העתק חלקי של נייר העמדה המקורי. הוא מתמקד בסגמנט הסביבתי של נייר העמדה (ה-"E" מתוך ESG). הטקסט המסומן בהטיה ובקו תחתון מהווה את עיקרי הדברים החשובים המצויים בו.

The EBA is part of the European System of Financial Supervision together with two other supervisory authorities

Published on 20/10/2020

Important: This article is a partial copy of the original EBA paper. This article focuses on the Environmental segment of the ESG (The "E").

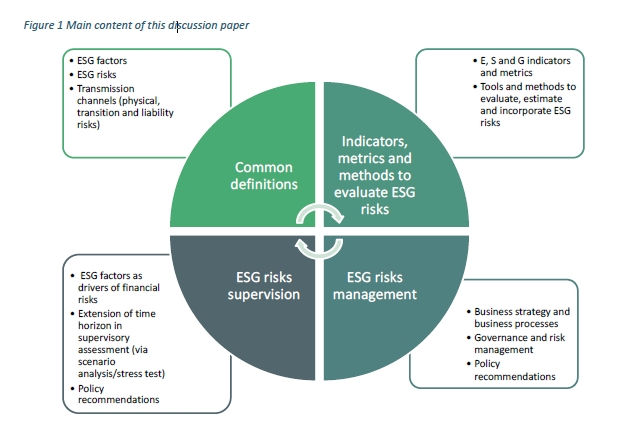

ESG factors materialise at many levels, such as international, country, sectoral or entity level. This discussion paper includes proposals for common definitions of ESG risks to credit institutions and investment firms (hereafter institutions) as risks that stem from the current or prospective impacts of ESG factors on its counterparties. Therefore, the financial materiality of ESG risks will need to be carefully assessed by institutions and supervisors. Since not all financing activities are likely to be equally affected by ESG risks, it is important that institutions and supervisors are able to distinguish and form a view on the relevance of ESG risks, following a proportionate, risk-based approach that takes into account the likelihood and the severity of the materialisation of ESG risks.

The main focus of this discussion paper is on the risks to which the institutions are exposed to via the impact of ESG factors on its counterparties.

In the discussion paper ESG factors and ESG risks are identified and explained, giving particular consideration to risks stemming from environmental factors and especially climate change, reflecting ongoing initiatives and progress achieved by institutions and supervisors on this particular topic over the recent years

The EBA sees the need for enhancing the incorporation of ESG risks into institutions’ business strategies, business processes and proportionately incorporate ESG risks in their internal governance arrangements. The EBA also sees a need to gradually develop methodologies and approaches to a climate risk stress test

discussion paper is closely linked with, and leverages on, the work done by other stakeholders, either policy-makers, central banks and the supervisory community, think-tanks, researches and industry initiatives.

In 2015, more than 190 governments around the world adopted the UN 2030 Agenda for Sustainable Development, aiming to support further progress on a wide range of many interconnected and cross-cutting economic, social and environmental objectives.

Also in 2015, signatories to the Paris Agreement committed to undertake ambitious efforts to limit the increase in the global average temperature to well below 2°C above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5° above such levels. This implies the need for early actions to reach peaking of greenhouse gas emissions as soon as possible and to undertake rapid reductions thereafter. In the long term, an unabated warming pathway would lead to significant declines in global GDP by 2100

The European Commission’s Action Plan has the following three main objectives:

a. reorienting capital flows towards sustainable investment in order to achieve sustainable and inclusive growth;

b. managing financial risks stemming from climate change, resource depletion, environmental degradation and social issues and;

c. fostering transparency and long-termism in financial and economic activity, and is complemented with broader legislative efforts to support the transition to a more sustainable global economy.

The financial sector is expected to play a key role in financing the transition of the economy to a more sustainable form. According to the EU Commission’s “Action Plan – Financing Sustainable Growth”, the financial system is being reformed to address the lessons of the financial crisis, and, in this context, it could be part of the solution towards a greener and more sustainable economy. Reorienting private capital to more sustainable investments was said to require a comprehensive shift in how the financial system works. This transformation will certainly spur new business opportunities, but the financial sector will also experience the financial risks stemming from the transformation of the economy and the worsening physical conditions.

The EBA report shall comprise at least the following:

a. a definition of ESG risks, including physical risks and transition risks related to the transition to a more sustainable economy, and, with regard to transition risks, including risks related to the depreciation of assets due to regulatory change, qualitative and quantitative criteria and metrics relevant for assessing such risks, as well as a methodology for assessing the possibility of such risks arising in the short, medium, or long term and the possibility of such risks having a material financial impact on an investment firm;

b. an assessment of the possibility of significant concentrations of specific assets increasing ESG risks, including physical risks and transition risks for an investment firm;

c. a description of the processes by means of which an investment firm can identify, assess, and manage ESG risks, including physical risks and transition risks;

d. the criteria, parameters and metrics by means of which supervisors and investment firms can assess the impact of short‐, medium‐ and long‐term ESG risks for the purposes of the supervisory review and evaluation process.

The impact of ESG risks materialises in the form of existing prudential risks (e.g. credit risk, market risk, operational risk).

Generally, references to ESG factors are associated with the concept of sustainable finance, sometimes also referred to as green finance. Specifically, sustainable finance relates to financing to ‘support economic growth while reducing pressures on the environment and taking into account social and governance aspects. Sustainable finance also encompasses transparency on risks related to ESG factors that may impact the financial system, and the mitigation of such risks through the appropriate governance of financial and corporate actors’.

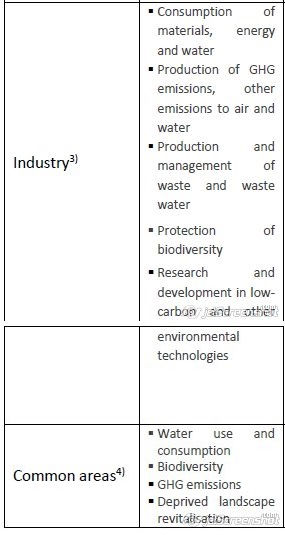

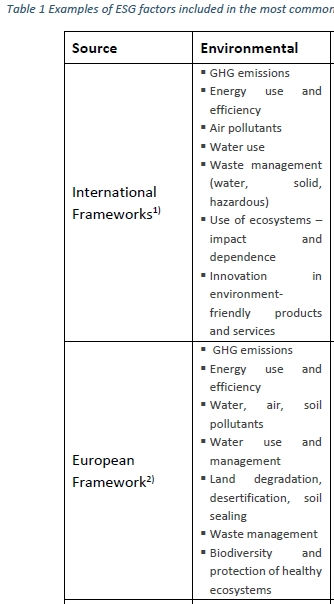

Examples of ESG factors that are common across those definitions and practices for financial and non-financial firms include greenhouse gas emissions, biodiversity and water use and consumption in the area of environment

Negative economic externalities: ESG factors such as pollution, overall welfare of the society, poverty, are of particular concern to the wider public. While they reflect the impact of a sum of individual activities, they are not captured in financial statements, meaning that the costs of those activities is borne by third parties or by the society at large and not fully captured by market mechanisms. For example, consider the ‘collective’ cost of greenhouse gas emissions generated by an entity. In the absence of carbon pricing that adequately captures climate related externalities, financial markets, while seemingly willing to price climate risk, are unable to fully reflect this risk in prices.

Patterns arising from the value chain: Patterns arising throughout the value chain mean the impacts from an entity’s activities and interactions with different stakeholders within its upstream and downstream value chains. In the context of these activities, an entity may face indirectly through its debtors and creditors different ESG factors.

Increased sensitivity to changes in public policies designed to mitigate climate change and other externalities: Signatories of SDGs and the Paris Agreement have committed to undertake ambitious efforts in meeting the set goals and targets, which imply major changes in public policies and regulatory framework. Efforts to limit climate change might imply significant regulatory shifts and lead into wider structural changes difficult to include into economic development predictions.

Example of public policies designed to mitigate climate change For example, at the European level, the EU’s Emissions Trading System (EU ETS) is key for the EU policy to tackle climate change and for a cost-effective reduction of emissions of carbon dioxide (CO2) and other greenhouse gases (GHG) in the power, aviation and industrial sectors. It was launched in 2005 and is the first – and still the largest – international system for trading GHG allowances covering over three-quarters of the allowances traded on the international carbon market, while it covers around 45% of the EU's GHG emissions. Another example is at national level, where the German legislator has adopted a law introducing a national emissions trading scheme for trading heating oil, natural gas, petrol and diesel. These mechanisms will significantly increase the price of fossil fuels in the construction and transport sectors and strain the profitability of corporates active in those sectors that are particularly dependent on fossil fuels.

The main purpose of this discussion paper is to define and develop assessment criteria for ESG factors that may impact the financial performance and solvency of institutions via their counterparties. For instance, an institution may experience a negative financial impact when it holds collateral assets that become stranded assets due to the introduction of regulatory changes aimed at containing climate change.

For the purpose of this paper, the ESG factors can be defined in the following way: ‘ESG factors are environmental, social or governance characteristics that may have a positive or negative impact on the financial performance or solvency of an entity, sovereign or individual.’

As referred to in the definition of the ESG factors, the ESG factors can have negative or positive impacts. From this perspective the ESG factors can be used also when evaluating opportunities for financial or non-financial entities related to the transition to more sustainable economy.

ESG risks materialise when the ESG factors affecting institutions’ counterparties have a negative impact on the financial performance or solvency of such institutions.

The materiality of ESG risks depends on the risks posed by ESG factors over the short, medium and long-term. In this regard, double materiality perspective in terms of the impact that the counterparty’s activities can have on the institutions’ performance can be identified and includes both:

a. financial materiality, which may arise from such economic and financial activities throughout their entire value chain, both upstream and downstream, affecting the value (returns) of such activities and therefore typically of most interest to institutions; and

b. environmental and social materiality, stemming from the external impact of those economic and financial activities, typically of most interest to citizens, consumers, employees, business partners, civil society organisations and communities.

When assessing financial materiality, it is also important to distinguish between impacts that are exogenous to the counterparty’s activities (e.g., floods, tsunamis, fires or other climate-related hazards) and impacts that originate from the counterparty’s activities (e.g. any activity that may be considered as damaging for the climate such as CO2 emissions or use of fossil fuels, and/or as a failure to comply with social standards, like labour conditions, and ethical values). Hence, managing ESG risks implies taking into account both types of materiality and the two potential originations of the impacts from ESG factors.

‘ESG risks mean the risks of any negative financial impact to the institution stemming from the current or prospective impacts of ESG factors on its counterparties’

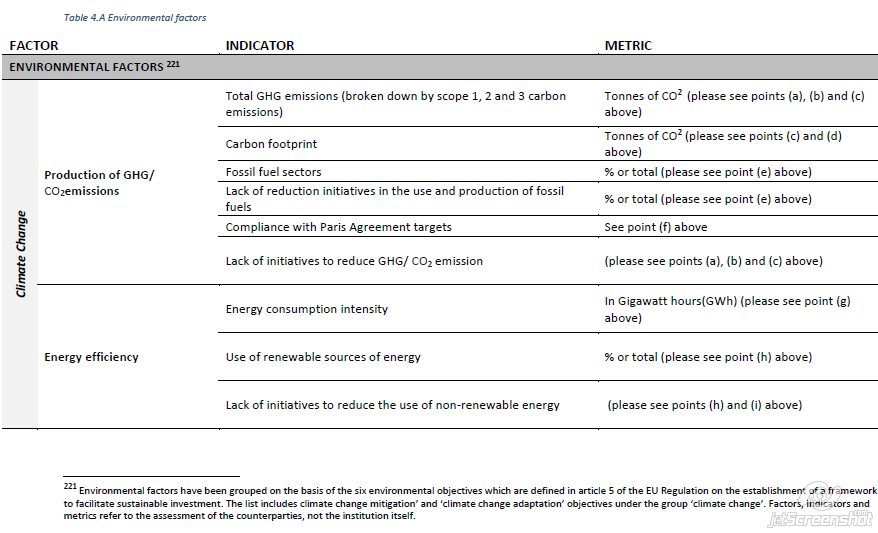

Environmental factors are related to the quality and functioning of the natural environment and systems, which may have an impact on the activities of the institutions’ counterparties. The main transmission channels for the impact of environmental factors cover physical (such as extreme weather events and gradually deteriorating conditions in climate) and transition (such as regulatory restrictions or taxation, disruptive technologies and changing consumer preferences) transmission channels. These channels can affect the entire value chain of companies as well as any other counterparties to which institutions are exposed.

The impact of environmental factors can be twofold, reflecting their potential double materiality. On the one hand, the financial performance of a counterparty can be affected by environmental factors, for example, the introduction of a carbon tax may decrease the profitability of carbon-dependent businesses or decrease the competitiveness of their products. On the other hand, the activities of the counterparties may have a negative impact on the environment, e.g., via the release of a large volume of CO2 into the atmosphere, leading to an environmental materiality, which may trigger a financial impact on such counterparties.

Environmental risks are driven by environmental factors. They should be understood as the financial risks posed by the institutions’ exposures to counterparties that may potentially contribute to or be affected by climate change and other forms of environmental degradation (such as air pollution, water pollution, scarcity of fresh water, land contamination, biodiversity loss and deforestation).

Climate-related risks are the financial risks posed by the exposure of institutions to counterparties that may potentially contribute to or be affected by climate change. For example, damage for companies or citizens caused by extreme weather events or a decline of asset value of a company in carbon-intensive sectors.

There is a connection and to some degree an overlap between climate-related and environmental risks. Climate change also leads to environmental degradation, as an increase of just 1.5°C is already expected to have a significant impact on biodiversity and ecosystems on land and in the sea. Yet, not all environmental degradation is a result of climate change as it can stem from other sources as well. For example, rising population levels and income growth leading to higher water demand will cause a large part of the world and its inhabitants to face water stress.

Climate-related and other environmental risk cannot be entirely separated, as they may reinforce each other given that climate change could increase the degradation of the environment and vice versa. For example, reductions in the diversity of cultivated crops due to the rise in temperatures may mean that agroecosystems are less resilient against future climate change, pests and pathogens. At the same time, healthy ecosystems contribute to resilience and adapting to conditions caused by climate change that are already taking place, such as higher temperatures, rising seas, fiercer storms, more unpredictable rainfall and more acidic oceans.

Therefore, the scope of the analysis presented in this discussion paper covers a definition of environmental risks that includes the impact of both climate-change and other environmental factors. For the purpose of this report ‘Environmental risks are the risks posed by the exposure of institutions to counterparties that may potentially be negatively affected by environmental factors, including factors resulting from the climate change and factors resulting from other environmental degradation.’

Environmental risks can materialise via the three main transmission channels:

a. Physical transmission channels

b. Transition transmission channels

c. Liability transmission channels (see section 4.6)

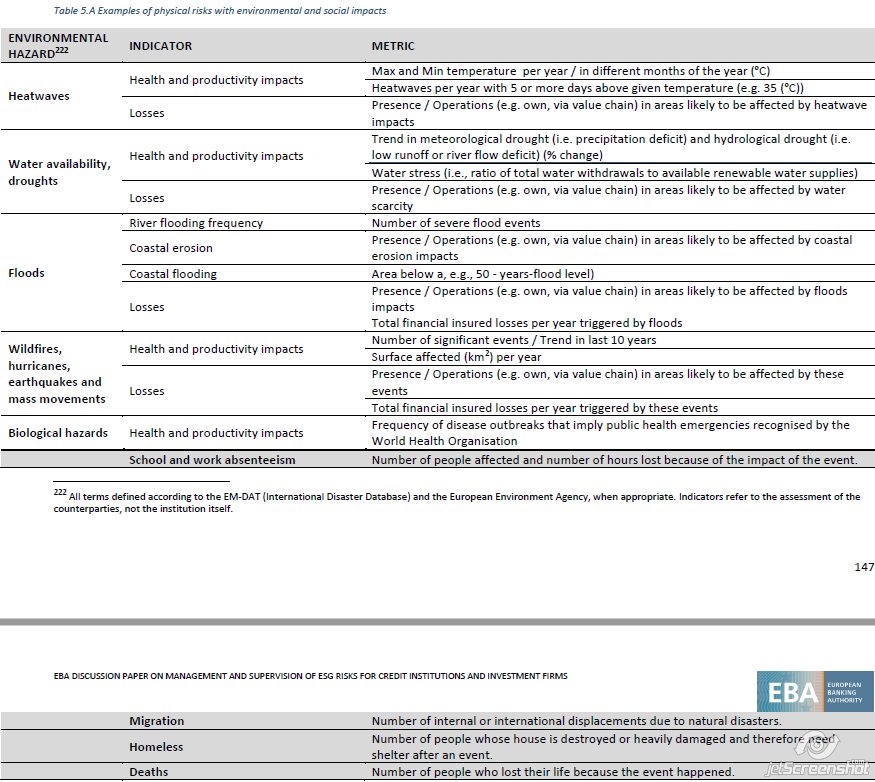

Although definitions of physical risks vary marginally among international organisations, central banks, supervisors, policy-makers and researchers, they are typically defined as one of the transmission channels through which climate-related risks (including shocks) can materialise, impacting negatively the financial position of counterparties and, hence, potentially causing the depreciation of assets.

For example, the ‘Guidelines on non-financial reporting: Supplement on reporting climate-related information’ issued by the European Commission define physical risks as ‘risks to the company that arise from physical effects of climate change. They include:

a. acute physical risks, which arise from particular events, especially weather-related events such as storms, floods, fires or heatwaves, that may damage production facilities and disrupt value chains;

b. chronic physical risks, which arise from longer-term changes in the climate, such as temperature changes, rising sea levels, reduced water availability, biodiversity loss and changes in land and soil productivity’.

So far, physical risks have been mainly defined as the impact or the transmission channels of climate change. However, there are environmental events other than climate change that can drive physical risks as well, such as water stress, biodiversity loss and pollution (see Box 3).

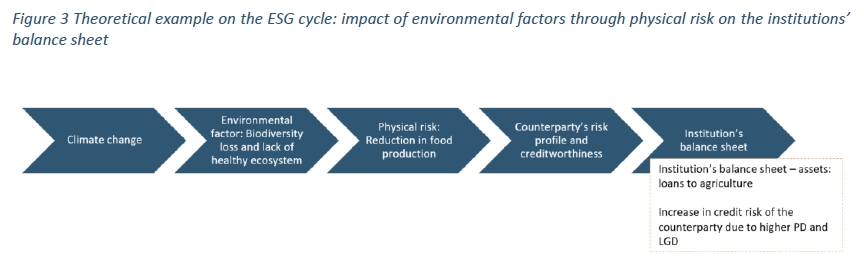

Figure 3 illustrates a cycle on how environmental factors (e.g. biodiversity loss and lack of healthy ecosystems) can manifest in environmental risk through the physical risk transmission channel and then have an impact on institutions’ balance sheet.

In this example, biodiversity loss impacts the risk profile of an institution’s counterparty, through the physical impact of a reduction in agricultural activities and food production. The physical impact transmits onto the balance sheet of an institution exposed to the agricultural sector, increasing its risk profile.

Considering the existing definitions of physical risks in the context of climate change, the EBA would extend this to environmental risks, defined as follows: Physical transmission channels/physical risks are the risks posed by the exposure of institutions to counterparties that may potentially be negatively affected by the physical effects of climate change or other environmental factors, including:

a. acute physical effects, which arise from particular events, especially weather-related events such as storms, floods, fires or heatwaves, that may damage production facilities and disrupt value chains; and

b. chronic physical effects, which arise from longer-term trends, such as temperature changes, rising sea levels, reduced water availability, biodiversity loss and changes in land and soil productivity.

Transition risks are the other main transmission channel through which climate change may impact the financial position of the institution’s counterparties negatively. Although definitions vary across different sources, transition risks generally refer to the uncertainty related to the timing and speed of the process of adjustment towards a low-carbon economy.

Such process will be affected, for instance, by the impact of the related policy action on the asset prices of carbon-intensive sectors and/or by physical risks themselves, and includes the risks of potentially disordered mitigation strategies. In addition, technological changes may, for instance, make existing technologies obsolete or could allow today’s comparatively less sustainable activities to become more environmentally friendly in the future. Such technological progress, if materialised, might trigger a repricing of assets that is difficult to foresee. Changes in the preferences and behaviour of consumers, investors and entities may also affect the relevance of ESG factors over time. As an example, a change in the preferences of customers (such as avoidance of investing in non-sustainable assets) may impact institutions’ investment product offerings.

The NGFS (Network for Greening the Financial System) defines transition risks as financial risks which can result from the process of adjustment towards a lower-carbon and more circular economy, prompted, for example, by changes in climate and environmental policy, technology or market sentiment.

The NGFS identifies three main categories of transition risk drivers in the context of climate risk:

a. Climate-related mitigation policies, which could lead to reductions in financial valuations and/or downgrades in credit ratings for companies not compliant with such policies because they no longer earn an economic return on past investment;

b. Technological advances, which could affect the relative pricing of alternative products and reduce the market shares of certain companies, resulting in lower profitability and eventually losses for institutions; and

c. Shift in public sentiment, demand patterns, and preferences and expectations that can affect the economy and the financial system.

In the European Commission’s ‘Guidelines on non-financial reporting: Supplement on reporting climate-related information’, transition risks (in the context of climate risk) are defined as ‘risks to the company that arise from the transition to a low-carbon and climate-resilient economy. They include:

a. Policy risks, for example as a result of energy efficiency requirements, carbon-pricing mechanisms which increase the price of fossil fuels, or policies to encourage sustainable land use.

b. Legal risks, for example the risk of litigation for failing to avoid or minimise adverse impacts on the climate, or failing to adapt to climate change.

c. Technology risks, for example if a technology with a less damaging impact on the climate replaces a technology that is more damaging to the climate.

d. Market risks, for example if the choices of consumers and business customers shift towards products and services that are less damaging to the climate.

e. Reputational risks, for example the difficulty of attracting and retaining customers, employees, business partners and investors if a company has reputation for damaging the climate.’

Another definition has been used by the TCFD (Task Force on Climate-related Financial Disclosure) in the context of climate risk, which identifies similar risk drivers, however grouped in four different categories: i) policy and legal risk, ii) technology risk, iii) market risk and iv) reputation risk.

Legal risks in the context of climate-change – sometimes also referred as liability risks or litigation risks – are often considered as a separate risk category and refer to the “the impacts that could arise tomorrow if parties who have suffered loss or damage from the effects of climate change seek compensation from those they hold responsible”. Legal risks are sometimes considered as part of either physical or transition risks, and are, in principle, more likely to impact on institutions that are active in the liability insurance market.

Transition risks can also impact individuals, for example, when they are employed by a carbon-intensive company that fails due to new carbon pricing mechanisms, and sovereigns, for example, when the transition causes mass unemployment and therefore a deterioration of tax income or increased public spending. They can also lower the value of collateral which does not meet the latest environmental standards or market expectations anymore.

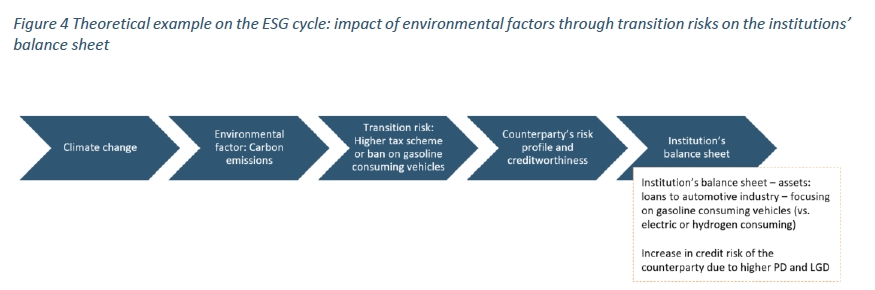

Figure 4 illustrates that regulatory intervention to tackle carbon emissions can create transition risk for the economic agents, and manifest as the counterparty risk on the institution’s balance sheet.

Such transition to a low carbon and climate-resilient economy, as mentioned above, can also provide opportunities for the counterparties -and the institutions providing funding to them – if companies contribute to climate mitigation and adaptation.

Similarly to the definition of physical risks, the existing definitions of transition risks are used primarily in the context of climate change. However, it can be easily expanded beyond climate change, e.g. to water stress and biodiversity loss, to cover all aspects of environmental risks (see Box 4).

In the case of water stress, policy risk bringing in regulatory changes may incentivise re-channelling of capital (and water) from less essential sectors and business activities (such as clothing industry) to more essential sectors and business activities (such as agriculture), affecting ongoing business operations of companies. Similarly, consumer behaviour and preferences as well as technological development may shift towards more water efficient practices.

Biodiversity loss can lead to policy risk when governments introduce measures to counter, for example, deforestation, use of fertilisers or excessive land use, which would then impact the value of businesses relaying on those lands or practices, or strict regulation in agriculture and fisheries affecting the outcome from those activities. Similarly, change in consumer dynamics and technology may shift practices towards more sustainable path ways to safeguard biodiversity.

Considering the existing definitions and main drivers of transition risks, the following definition, extended to overall environmental risks, is proposed. Transition transmission channels/transition risks are the risks posed by the exposure of institutions to counterparties that may potentially be negatively affected by the transition to a low-carbon, climate-resilient or environmentally sustainable economy, including:

Transition and physical risks interact closely with each other and companies and institutions may be subject to the full impact of these risks.

The persistent emissions of greenhouse gases without carbon removal technologies in place and the continuation of unsustainable practices in the economy contribute to the very source of physical risks, potentially exacerbating the likelihood of environmental hazards and its socio-economic impacts.

As a response to the impact of physical risks, policy makers will likely introduce, where not already in place, mitigation policies and regulation; people’s preferences may also change towards more sustainable products and services. As a result, the negative impact of both physical risks and transition risks is more likely to materialise. For example, an institution might be exposed to counterparties that go bankrupt due to the introduction of climate mitigation policies, while at the same time assets held as collateral are damaged during a flood incident.

In addition, depending on their scale, physical and transition risks have the potential to trigger significant impacts on the real economy and the financial system as a whole. These impacts may result from natural disasters and other environmental hazards and from the policies implemented in order to prevent or moderate the deterioration of the environment and climate change. As an illustrative example, continued environmental deterioration will impact the aggregate output levels as well as potential growth rates, as some economic activities become unviable or labour conditions deteriorate due to health issues. This could be the case, for instance, when rising temperatures and changing patterns of precipitation directly impact industries, such as agriculture and fisheries, energy, tourism, and construction among others. The relative adjustment of prices in the economy that will need to take place may create additional disruptive effects and further exacerbate the level of uncertainty, potentially increasing social unrest, as the impact of physical and transition risks is likely to be unevenly distributed across populations. Ultimately, further global warming could impact the solvency of sovereigns whose economies are heavily dependent on sectors vulnerable to climatic changes, such as agriculture or the tourism sector. While such significant macroeconomic impacts may occur in the more distant future, some impacts are already evident.

Social factors are related to the rights, well-being and interests of people and communities, which may have an impact on the activities of the institutions’ counterparties. Social factors, such as (in)equality, health, inclusiveness, labour relations, and investing in human capital and communities, are increasingly being considered in the business strategies and the operating frameworks of businesses, institutions and their counterparties.

Environmental and social risks are closely interrelated (see Box 5). The continuous deterioration of environmental conditions implies heightened social risks, such as when climate-related physical change or water stress affect deprived parts of a geographical area and already disadvantaged populations. Environmental degradation can exacerbate migration, social and political unrest in the most affected regions, with potentially more devastating repercussions and contagion across the globe. According to the Internal Displacement Monitoring Centre, between 2008 and 2018, natural disasters displaced as many as 265 million people. The World Bank projects that by 2050, lower water availability and crop productivity combined with the impact of other physical risks like storms or rising sea levels may lead 140 million people to migrate within their countries in Latin America, South Asia, and sub-Saharan Africa. While global warming should not be held solely responsible for migration decisions, it may amplify existing motivations such as income inequality, lack of human rights or civil wars. Another example of the interconnection between environmental and social risks is the potential impact that envisaged technological and regulatory changes to combat climate change may have on labour markets, for instance, amplifying social risks, particularly for (non-green) industries where low-skilled labour is prominent, e.g., the coal mining industry. The timing for the potential manifestation of these social risks is uncertain.

The outbreak of the COVID-19 pandemic provides a good example of the interaction between environmental, social and governance factors. Several commentators have highlighted the importance of biodiversity loss in the origin and spread of new diseases with several health and social impacts.

For the purpose of this discussion paper, “Social risks are the risks posed by the exposure of institutions to counterparties that may potentially be negatively affected by social factors.”

Governance plays also a fundamental role in ensuring the inclusion of environmental and social considerations by a given counterparty. Recognition of the potential impact of climate and environmental changes and related physical, transition and liability risks is understood as a sign of good governance. To the contrary, neglecting these potential impacts in the strategic planning of a counterparty may create additional governance risks.

There can also be a correlation between poor environmental performance and poor governance as evidenced by the Diesel emissions scandal. A small number of car manufacturers had declared for years lower-than-real nitrogen oxide emissions to the licensing authorities and their customers. The low values were made possible by a setup of the engines that could distinguish between test mode and normal operations. In test mode, the engines were electronically manipulated in order to only produce emissions below accepted thresholds. The scandal was disclosed by a Notice of Violation by the US Environmental Protection Agency and costed the German car manufacturer Volkswagen USD2.8bn in fines and about USD17bn in damages in the US alone.

For the purpose of this discussion paper, “Governance risks are the risks posed by the exposure of institutions to counterparties that may potentially be negatively affected by governance factors”.

Another transmission channel of ESG risks that is often stated in discussions on ESG factors is liability risk. Liability risk relates to the risks stemming from people or businesses seeking compensation for losses they may have incurred due to ESG factors, e.g. when institutions’ counterparties are held accountable for the negative impact through their activities on the environment, the society and their governance factors.

For the purpose of this discussion paper, “Liability transmission channels/liability risks are the risks posed by the exposure of institutions to counterparties that may potentially be held accountable for the negatively impact through their activities on the environment, the society and their governance factors.”

Multi-point impact of ESG risks on institutions:

Given that ESG risks can drive different prudential risk categories, they can impact the financial position of institutions in multiple ways. For instance, the physical deterioration of areas in which some economic activities (e.g. agriculture, construction) operate may lead to higher credit losses, if an institution is exposed to those activities via loans or bonds, or losses in market value, where the exposure is in the form of financial instruments. The necessary and politically agreed transition towards a more sustainable economy in general, and a carbon-neutral economy in particular, can also negatively affect existing business models. Credit and market losses translate into impacts on the capital adequacy and, thus, prudential soundness of an institution. Moreover, when credit agencies include ESG risks, the credit ratings of vulnerable corporates could be downgraded resulting in higher risk weights of affected exposures under the standardised approach. In addition, when ESG risks impair the valuation of collateral, this can increase the LGD. ESG risks can also cause an outflow of capital, for example, after a natural catastrophe. With regard to the costs of capital and funding, investors and depositors are likely to discriminate increasingly against institutions that disregard the negative effects of their activities on ESG factors.

The Second Annual Global Survey of Climate Risk Management at Financial Firms conducted by GARP found that the vast majority of institutions believes climate risk is either only partially included in pricing or even completely omitted. The publications of the ECB’s draft supervisory expectations relating to risk management and disclosure of climate related and environmental risks in May 2020, the NGFS’ ‘Status Report on Financial Institutions – Experiences from working with green, non-green and brown financial assets and a potential risk differential’ and the EBA Staff Paper on ESG Market Practices, further highlight the importance and urgency of enhancing the tools and methods for assessing and measuring ESG risks.

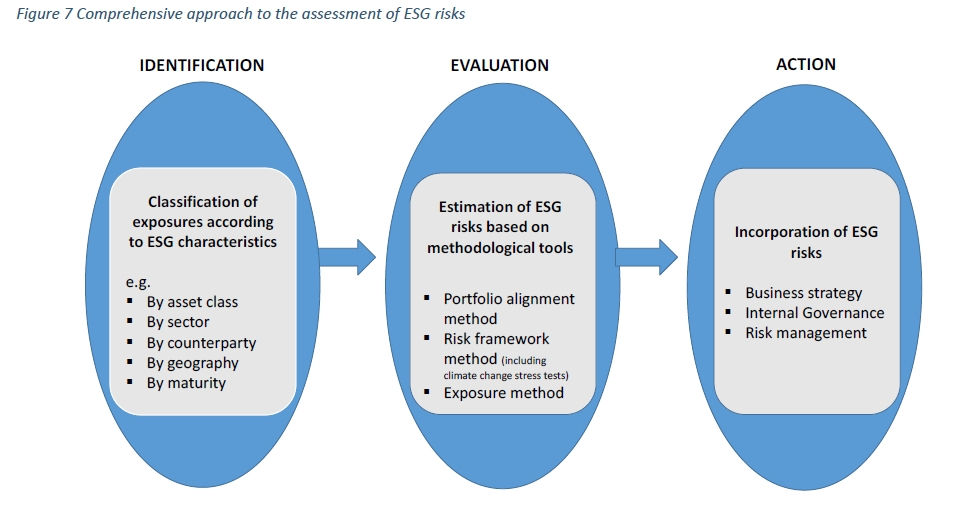

In this section, specific aspects relevant for the assessment by institutions and supervisors of ESG risks are presented. Section 3 focuses on two aspects of the risk management framework, namely the (i) identification and (ii) evaluation of ESG risks, as needed for the incorporation of these risks into the institutions’ decision-making (see Figure 7). Section 4 will elaborate more on the element of action. Specifically, the three elements can be depicted as follows:

a. Identification: This implies classifying assets according to their ESG characteristics in order to support the identification of ESG risks based on specific qualitative and quantitative indicators. This can be done, for example, through the categorisation of exposures (if applicable combined) across asset classes, sectors, counterparties, geographies or on the basis of their length of maturity or position in the life cycle of the asset. For instance, a geographic classification would help to identify the proportion of assets particularly vulnerable to the impact of physical risks in the form of higher sea-levels, droughts or other climate-related hazards in given regions, while a sector classification could be used to enhance the understanding of the share of exposures vulnerable to transition risks, for instance, in the form of regulatory changes and technological progress affecting those specific sectors. This classification process allows to identify the main potential drivers of ESG risks, consistent with the significance of the different ESG characteristics, which then justify a more granular analysis on the most relevant categories (e.g. a given geography, sector), if needed.

b. Evaluation: Once exposures have been classified, methodological tools would need to be applied and possibly combined to assess the potential impact of ESG risks on the institution’s ‘portfolios’. Given that methodologies to quantify ESG risks are evolving, a dynamic, flexible approach would be needed. For instance, some methodologies could fit well for the evaluation of ESG risks in exposures that are potentially vulnerable to misalignment with sustainable goals, like in the case of sovereign and public debt held by countries or regions that fail to comply with the Paris Agreement goals, while other methods may be needed to evaluate ESG risks stemming from the specific ESG-related features of a given counterparty (e.g. the labour code applied by a given company or the level of corruption in a given country).

Some ESG indicators, particularly those applicable to climate-related and environmental factors, are well-known and potentially fairly simple to calculate and apply. For instance, in the context of climate change, indicators for the production of greenhouse gas emissions are well-defined and can be measured, reported and verified with a high level of accuracy based on existing standards. Specifically, the ISO 14064-1:2018 standard applies a GHG Protocol methodology. In addition, the European Commission’s Recommendation 2013/179 on the use of common methods to measure and communicate the life cycle environmental performance of products and organisations provides further guidance on the use of environmental footprint methods.

At the European level, the European Commission’s ‘Guidelines on non-financial reporting: Supplement on reporting climate-related information’ from June 2019, which integrate the recommendations of the Financial Stability Board's TCFD, provide a starting-point for some climate-related indicators. Moreover, the EU Taxonomy Regulation classifies environmentally sustainable economic activities based on uniform criteria.

The EU Taxonomy provides a starting point for the uniform identification and classification of economic activities that are conducive to a low-carbon, resilient and resource-efficient economy. The Taxonomy Regulation provides a harmonised set of criteria to identify environmentally sustainable economic activities, including enabling and transition activities (see Box 9). An explicit objective behind the establishment of the EU Taxonomy is to support the reorientation of capital flows towards sustainable investments.

The six environmental objectives covered by the Taxonomy Regulation are (1) climate change mitigation, (2) climate change adaptation, (3) sustainable use and protection of water and marine resources, (4) transition to a circular economy, (5) pollution prevention and control, and (6) protection and restoration of biodiversity and ecosystems.

On the one hand, the Taxonomy encompasses economic activities that make a substantial contribution to one of those environmental objectives based on their own performance, i.e. straightforward sustainable activities. On the other hand, the Taxonomy also recognises so-called “enabling activities”. These are the provision of products or services to other economic activities which then make a substantial contribution, e.g. the production of parts for a carbon-neutral power plant.

Compliance with the taxonomies and standards has supported the development of labels, which consist of certified accreditations that formally recognise compliance of financial products with given taxonomies and standards (for instance, for the issuance of a ‘green bond’, for the granting of an ‘energy efficiency mortgage’, etc.). Finally, in order to promote the integration of markets for green financial products globally, the EU has launched together with seven other countries the International Platform on Sustainable Finance (IPSF) with the aim of ensuring a global coordination of efforts on initiatives and approaches to sustainable finance, in particular regarding labels for sustainable financial assets, including green bonds.

On 17 July 2020, the European Commission adopted new rules setting out minimum technical requirements for the methodology of EU climate benchmarks. The new rules increase the level of transparency and comparability on the products developed by benchmark administrators, including the criteria for the benchmarks to be labelled as EU Climate Transition Benchmark or EU Paris-aligned Benchmark.

While providing the starting point for the identification of ESG risk, taxonomies and indicators by themselves are not sufficient for the estimation and evaluation of ESG risks (see Figure 7 above). Various methods exist for using and translating them into an assessment of ESG risks. Ultimately, all approaches have the same objective of assessing the alignment of institutions’ portfolios with global sustainability goals and offering insights into the risk caused by exposures to certain sectors (for example, to climate relevant sectors). However, there are different ways of achieving these objectives. Each approach is different in terms of what it measures and how the outcome can be used by institutions. The decision on which methodological approach to choose will also depend on the size, the complexity and the business model of the respective institution and consequently the approach taken by a small, non-complex institution will likely differ from the one taken by a large institution.

In what follows, methods for assessing ESG risks are divided into three different types of approaches:

a. Portfolio alignment method

b. Risk framework method (including climate-stress test)

c. Exposure method

For all methods described, the well-known issue of data gaps and often lack of reliable and comparable data applies and has to be kept in mind.

How aligned is an institution’s portfolio relative to global sustainability targets?

At the core of this methodological approach is the concept of alignment. The key principle behind this approach is for institutions, investors and supervisors to understand in how far portfolios are in line with globally agreed (climate) targets.

Looking specifically at climate, this approach outlines in how far an institution would need to change its portfolio and activities in order to align with the Paris Agreement 2 degree scenario. It looks directly at the ultimate goal of global efforts on climate change and explicitly defines the portfolio changes that would be required by institutions to contribute to this. Assessing the alignment of the portfolio with global targets in turn presents a way to measure ESG risk for the bank itself.

A well-known tool falling under this approach is the Paris Agreement Capital Transition Assessment (PACTA) tool developed by 2 Degrees Investing Initiative (2DII). The tool combines bank level portfolio information on client exposures, a database on the technology mix and production plans of individual companies and technology mix scenarios developed by the International Energy Agency (IEA) in order to assess an entity’s alignment with the Paris Agreement Targets (bringing the rise in temperature to well below 2 degrees).

The technology mix scenarios define pathways for CO2 emissions for certain technologies and industries, under various climate target scenarios, implying certain required technology mixes in the energy sector. The 2DII database holds information on the production plans of individual firms for the period 2019-2024 for climate relevant sectors. Production plans by individual firms together with the envisaged scenarios’ pathways for different sectors are combined to assess the alignment of each firm’s production plan to the scenarios developed by the IEA.

At the bank level, each client exposure is matched with the 2DII database on firms and their forward-looking production profiles is created. Individual institutions can then be assessed in how far the clients they finance are aligned to the International Energy Agency (IEA) targets.

The output of PACTA provides institutions with the following: i) how much of the portfolio consists of clients in transition relevant sectors, showing the share of the portfolio and the technology mix of the portfolio; ii) a comparison of step i) to peers and the market (i.e. exposure of the global universe of assets in the relevant asset class); iii) the alignment of the bank’s portfolio to the scenarios over a 5 year horizon, based on the production plans of clients in its exposure. (The tool can of course can also be used by other financial sector entities, such as insurers and asset management companies.)

Another framework that takes the alignment approach is UNEP FI’s Principles for Responsible Banking (PRB), launched in September 2019 by 130 banks from 49 countries. The aim of this framework is to ‘align banks’ business strategy with the goals as expressed in the SDG and the Paris Agreement. A key difference of this framework compared to the PACTA approach is that it takes into account all three components of ESG, not only the environmental component. Twenty-two ‘impact areas’ are defined in line with UNEP FI’s Positive Impact Initiative 2018 in the social, the environmental, the governance, as well as the economic pillar. Each impact area can be mapped to at least one of the 17 SDG's.

The tool allows a mapping of participating banks’ exposures (by type, country and sector) to the different impact areas. The outcome is an overview for each bank in how far its exposures are positively or negatively affecting each impact area. Importantly, it builds a bank-specific list of most significant impact areas per bank. This is based on countries’ needs in each impact area for the bank’s countries of operation as well as impact areas related to sectors and countries where the bank is a market leader. Combined with an assessment of a bank’s (relative) performance on these most significant impact areas, the tool allows banks to set targets for each individual impact area.

The tool under the PRB is not based on quantitative scenarios like the PACTA Tool. Rather it provides a more qualitative mapping of the above-mentioned ‘impact areas’ to sectors and individual countries’ level of need. It involves subjective judgement both on the side of banks (when mapping the performance on most significant impact areas) and UNEP FI (when linking sectors with impact areas). Its all-encompassing scope of ESG and its differentiation across countries and banks’ own potential in the various impact areas, allows a holistic analysis on banks’ portfolios.

Signatory banks of the PRB are required to publish their targets, report publicly on their impacts and progress and engage with key stakeholder on their impacts, fostering transparency and accountability.

How will sustainability related issues affect the risk profile of a bank’s portfolio and its standard risk indicators?

Modelling the impact of ESG risks on banks’ risk profiles has seen most progress in the form of climate stress testing. This may inter alia be attributed to the fact that climate risk by its nature is forward-looking. Stress testing over a future horizon is therefore a useful tool to model climate risk impacts.

The most developed risk framework methods in the context of climate risk can be split into two approaches:

a. Climate stress tests – assessment featuring fully fledged scenarios that map out possible future development paths of transition variables (e.g. carbon prices), physical variables (temperature increases) and the related changes in macro variables (e.g. output in different sectors, GDP, unemployment) and financial variables (e.g. interest rates). These scenarios are then translated into changes in portfolios’ (risk) attributes.

b. Climate sensitivity analysis – a simpler exercise without scenarios, assessing changes in portfolios’ risk attributes by changing some of the inputs in financial models based on shading and classification of exposures into ‘green’ versus ‘non-green’ (which determines an exposure’s vulnerability to climate-related events and policies).

a. Climate stress testing

Several climate stress-testing methodologies have been proposed and applied. Stress testing can take place at portfolio, industry or counterparty level. Challenges include assumptions made about the different climate scenarios, uncertainties about climate developments themselves (tipping points), environmental policies adopted by national and international governments/bodies and actual implication for financial and economic factors and how these are modelled, choosing appropriate time horizons (which are longer for climate stress tests than for normal stress tests), taking into account transition or physical risk, accounting for changes in technology and consumer preferences, and, importantly, data availability.

Climate stress tests remain work in progress and should not be expected to provide the same level of precision as standard bank stress tests. To-date they remain of less comprehensive nature than the usual stress tests – they are an assessment of certain portfolios but do not make any conclusions about potential capital implications. Climate stress tests based on scenario analysis are a useful and important tool, however given their complexities and many uncertainties, they also need to be assessed and interpreted with caution.

Stress tests have also been developed for environmental stress such as pollution. Other stress tests are developed explicitly for the real estate sector, given its crucial contribution to climate change but also its exposure to physical risk.

b. Climate sensitivity analysis

Sensitivity analysis is a simpler form to integrate climate risk into financial risk modelling. It does not apply complex scenarios based on assumptions on time horizons and interlinkages between climate factors and the real economy, but instead integrates climate risk directly into financial risk indicators by stressing certain inputs, based on classifying exposures according to their positive or negative climate contributions.

Not requiring complex scenario based modelling can be seen as an advantage as it makes this approach simpler and more accessible. What it cannot provide however is a more dynamic and complex assessment of climate impacts. By definition, scenario analysis ignores many aspects, including the dynamics and interactions between different sectors, additional macroeconomic impacts resulting from climate change, and importantly it ignores negative feedback loops and the aspect of time (it is a one-point in time assessment).

Given the infancy of and uncertainties involved in climate risk modelling, this simpler approach can provide an insightful indication of the relative performance of ‘green’ versus ‘non-green’ exposures and banks’ exposures to climate relevant sectors.

How do individual exposures and clients perform in terms of ESG risk?

The third approach is a tool that banks can apply directly to the assessment of individual clients and individual exposures, even in isolation. The basic principle of this approach is to directly evaluate the performance of an exposure in terms of the E, the S and the G. This can then be used to complement the standard assessment of financial risk categories. Indicators used for this assessment are typically calibrated at company level, taking into account granular sectoral level characteristics to capture specific sensitivities of the ESG factors on different segments and sub-segments of economic activities.

This method can be described as the possibly most practical method and the most straight-forward to implement amongst the three approaches. It does not involve sophisticated scenario analysis based on many assumptions, but as a result relies on mainly backward-looking metrics. It can be applied to individual exposures and is a systematic approach classifying exposures by their specific ESG attributes. It provides banks and investors with a tool to better understand their individual counterparties and to better understand the ESG risk of their existing portfolio.

Several methodologies have been developed under this approach. They can be broadly classified into the following:

a. ESG ratings provided by specialised rating agencies (e.g. Sustainalytics, MSCI, ISS ESG, RobecoSam)

b. ESG evaluations provided by credit rating agencies (e.g. S&P’s ESG evaluation)

c. ESG evaluation models developed by banks in-house for their own assessment

d. ESG scoring models developed by asset managers and data providers, publicly available (e.g. State Street’s R-Factor, Refinitiv)

ESG ratings provided by specialised rating agencies are direct, stand-alone ratings on ESG factors, taking into account risk exposure to ESG factors as well as management’s capability to deal with risks or opportunities. These ratings can be either relative to industry peers (see MSCI ESG Ratings for instance) or absolute company ratings (see the rating by Sustainalytics). The methodologies generally build on quantitative analysis of key issues identified per industry (and hence company), as well as qualitative information collected by analysts from public information and client engagement.

All ESG evaluations aim to provide the needed additional input to existing financial risk assessment. Developing and interpreting the outcomes however also faces several challenges since the different approaches taken can have crucial implications for their comparability. For instance, ESG ratings often lead to very different outcomes for the same company. This is inter alia due to the fact that the importance of the same ESG factor for the same company is often assessed very differently across methodologies. Other factors contributing to the difficulties in comparing ESG ratings by different providers include the different weightings applied to the individual elements ‘E’, ‘S’ and ‘G’, whether, for instance, when looking at scope 1, 2 or 3 emissions for the E factor, or at the different treatment of lack of disclosure of information by companies.

A key step towards making ESG ratings and evaluations more comparable, transparent and as such more effective in their use, is a standardisation of the relevance and importance of different ESG factors for the various industries and companies. This direction has been taken by the Sustainability Accounting Standards Board (SASB), making a crucial contribution towards laying the basis for achieving consistency in ESG assessments (see Box 13).

The SASB has developed a publicly available Materiality Map, identifying financially material ESG issues for 11 sectors and 77 industries. Financially material factors are those that are likely to have a substantial impact on a company’s financial and operational performance. By nature, which ESG factors are material for a company depends on the company’s sector. The aim of the materiality map is to foster a common understanding of the relative importance of different ESG factors across various industries, thereby facilitating a consistent assessment of ESG risk.

The materiality map is complemented by Sustainable Accounting Standards. The latter identifies which factors should be reported and assessed to evaluate ESG performance. It provides as list of indicators relevant for a certain industry (such as for example the percentage of active workforce covered under collective bargaining agreements to assess labour force practices) and the rationale alongside this.

Whilst the SASB’s tools do not provide a direct ESG rating or scoring, they have the potential to play an important role in developing these. Providing a list of standardised ESG issues across industries and sectors permits consistent application by banks and investors for their ESG assessment of clients and portfolios and at the same time can be a signalling tool for companies to identify the areas they should focus on in order to improve their sustainability performance.

https://www.sasb.org/

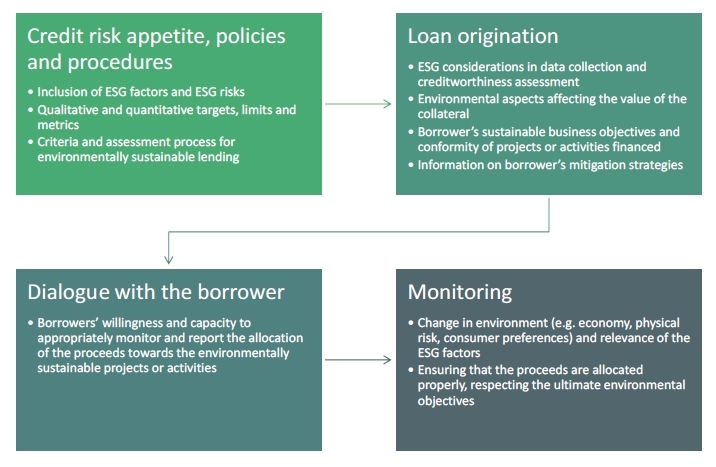

The EBA Guidelines on Loan Origination and Monitoring specify that ESG factors should be taken into account in banks’ credit risk appetite, policies and procedures. In particular, the Guidelines outline specific processes and procedures banks should have in place when providing environmentally sustainable lending, including processes for assessing the credibility and business objectives of clients.

Portfolio monitoring in the context of ESG in turn is crucial as it allows the bank to spot difficulties and areas for concern and action early on and allocate capital accordingly. In particular, it enables an institution to gain experience and build historical data on ESG and the relative performance of portfolios, which is again critical for the future policies and strategies of an institution.

Exposure origination

Alignment Method – Understanding the state of alignment and potential for changes in the portfolio provides direction and allows for better-guided decisions on investment and sectoral focus at time of exposure origination. The method focuses more on assessing the exposure in the context of the entire portfolio composition.

Risk Framework Method – Stress testing or sensitivity analysis can provide insights into vulnerabilities of sectors for future investment or credit decisions. It can help inform appropriate pricing and term structure of a loan and make portfolio allocation decisions.

Exposure Method – Providing a detailed view of ESG issues by client, the exposure method seems appropriate for the screening conducted during the loan origination process. In particular because ESG evaluation can be available at company level, it allows for a detailed and customised assessment of clients.

Portfolio monitoring

Alignment Method – Understanding the positioning of a portfolio relative to targets allows identifying which parts of the portfolio are most likely to encounter difficulties in the future and require hence more attention and which portfolios may even need to be divested.

Alignment Method – Some methodologies can guide dialogue with client companies (through its insights on individual companies’ investment and production plans).

Risk Framework Method – Understanding the impacts of climate on the portfolio’s risk parameters is a crucial input to portfolio monitoring and capital allocation.

Exposure Method – It requires a substantial amount of evaluation in retrospect, but can be a useful tool for banks to understand in detail how their portfolio performs on ESG factors (‘shading of the portfolio’), can guide dialogue with clients and directs the latter on how and where improvements need to occur. This allows for a very customised tool.

Exposure Method

Pro's

Con's

Building on the definitions of ESG factors, ESG risks and their transmission channels, this chapter addresses how institutions can embed ESG risks in their governance and risk management. After describing the main practices currently followed by institutions (section 6.1), this chapter is structured around the three main elements where the incorporation of the ESG risks is seen as essential:

a. business strategies and business processes (section 6.2),

b. internal governance (section 6.3) and

c. risk management (section 6.4).

Smaller institutions are not immune to ESG risks and could be even more susceptible to them, for instance, if they are particularly concentrated in a vulnerable sector, geography or if they lack the resources and expertise needed to manage ESG risks. This is why it is important that all institutions effectively identify and monitor the ESG risks to which they might be exposed in the short, medium and long-run, and that they implement adequate measures to address them.

Incorporating ESG risks into institutions’ activities can be a complex task. Managing ESG risks requires a specific, long-term, forward-looking and comprehensive approach, which is at the same time flexible enough to account for ongoing developments in terms of the integration of ESG risks into the institutions’ business and risk management processes.

some credit institutions are accounting for ESG risks as more immediate financial risks in their business strategies and have decided to adapt risk management frameworks accordingly. Practical steps taken to achieve this objective included, among others:

a. DNB’s good practices publication in 2020 provides insights into how such a strategic approach to climate-related risks was adopted by one credit institution. In this case, an internal change program was introduced to understand the risks from climate change arising for the institution, the strategy was reviewed for necessary adaptions and the decisions subsequently implemented. In addition, and partly combining CSR and financial risk focuses, some credit institutions also reported in the EBA survey that they evaluate the impact of their lending, engage with clients about ESG risks, setting objectives for the share of investments that would need to meet positive ESG criteria or offering products such as green bonds or loans. Lastly, selected credit institutions have focused their business model on sustainability, declaring a significant importance of ESG considerations to their business strategy.

b. According to the above-mentioned PRA survey, around 60% of the respondents had adopted the approach of considering climate-related risks as more immediate financial risks, albeit in a mostly rather narrow and short-term fashion. Another 10% were found to have chosen a more comprehensive, “strategic” approach, including a more long-term, forward-looking perspective, developing asset classifications for climate-related risk analysis and increased board engagement as well as engagement with academia or hiring of specialists. The study conducted by the ACPR also confirms progress with regard to the integration of climate-related risk into institutions’ strategies and observes “advanced institutions” that have increased efforts in terms of quantifying climate-related risks, reviewing sectoral policies or aligning portfolios with climate change mitigation scenarios to reduce exposure to transition risks.

The EBA report on short-termism shows that the average time horizon for business planning and strategy setting considered by EU banks is currently three to five years, which is also in line with the time horizon required by some supervisory requirements. However, this time horizon is not likely to immediately reflect the often long-term impacts of climate change nor the transition to a more sustainable economy, e.g. in line with the objectives of international agreements, and may make them seem less relevant for institutions. Accordingly, the report concludes with a recommendation to integrate “requirements to implement long-term resilient business strategies” into the EU-level provisions, such as the CRD, for the banking sector.

The above-mentioned EBA’s survey conducted in 2019 showed that a growing number of credit institutions are working on determining the materiality of ESG risks. Although credit institutions assess climate-related risks (including both physical and transition) to be potential material risks for their activities, credit institutions’ current efforts to put in place specific risk management processes in relation to climate-related risks are limited. In particular, it appears that credit institutions have neither yet established key performance indicators that are necessary for a robust internal risk review process, nor more sophisticated modelling approaches.

The EBA findings are broadly in line with the evidence found by other surveys focusing mostly on climate-related risks only. Notwithstanding ongoing efforts and the progress made, most available studies and surveys call for a more assertive integration of climate risks as a financial risk, hence moving beyond a pure reputational risk focus.

The European banking sector has a long way to go in terms of addressing climate-related risks. While the surveyed banks have become much more transparent on their approaches to climate change in line with the TCFD recommendations, the sector performs the most poorly in terms of risk assessment and management of climate risks.

In May 2020, GARP Risk Institute published its second Global Annual Survey of Climate Risk Management at Financial Firms. In the survey, 85% of the 71 institutions show concerns over their resilience to climate change beyond 15 years. The main barriers to address climate risks mentioned by the respondents relate to the availability of reliable models and regulatory uncertainty, especially in the short term. In addition, most firms state that getting internal alignment on their climate risk strategy is a challenge in the short term.

Exclusion criteria on certain sectors and exposures are tools that institutions have begun to consider in their risk policies and risk management framework. Indeed, the findings of the EBA market practices survey shows that some credit institutions consider both positive and negative impacts of their investments and take those impacts into account for their financial decisions.

Asset managers use a number of approaches for the purposes of selecting exposures and implement sectoral exclusion policies:

a. Exclusion: the entity excludes from its investment range controversial assets (for example, negative environmental or social impact, corruption affairs) that do not match a minimum non-financial score established by an internal methodology designed by the entity;

b. Best-in-class: the entity is ranking companies by sector with an internal methodology (for example by GHG emissions) and allows for investment only, for example, in the three first companies in every sector. No economic sector is ignored using this approach;

c. Best-in-universe: the entity rank all the assets in its investment range using an internal methodology (again for example entities can be ranked on their GHG emissions) and is only choosing to invest in the assets ranked best. This can lead to ignore certain economic sectors;

d. Best-effort: the entity is choosing to invest in companies that have shown the best improvements regarding ESG factors (e.g. biggest GHG emissions reduction). Hence, these companies are not necessarily the best in terms of “absolute” ESG indicators;

e. Impact: the entity is selecting specific companies that have a positive impact regarding ESG criteria previously defined by the entity, e.g. a start-up developing an innovative ecological solution;

f. Normative: the entity is selecting investments regarding their compliance with international norms and standards.

From a prudential point of view, there are sound reasons for institutions to take ESG risks into account when assessing, designing or modifying their business strategy and processes. Notwithstanding the negative impacts from ESG risks that already occur in the short and medium-term, it is likely that the full impact of ESG risks will unfold over a longer time horizon. Therefore, if ESG risks are not duly taken into account in their business strategies, institutions might fail to modify their business models in a timely manner to avoid or mitigate the longer-term impacts of ESG risks.

Considering the relevance and potential impact of ESG risks, including them in the institution’s business strategy and business processes could be seen as inevitable for the institutions’ economic resilience over the long-term. By steering business into a direction that is consistent with the expected environmental and social transformation, institutions are more likely to avoid the negative impacts from ESG risks.

The UN 2030 Agenda for Sustainable Development and the Paris Agreement could be considered as the main global reference documents outlining commitments and vision for transforming the current global economy into a more sustainable one. In the EU context, the European Commission’s proposal for the so-called ‘European Climate Law’ sets the direction of travel for EU policy together with a more specific ‘Action Plan: Financing Sustainable Growth’. These have been supplemented by the Communication on the European Green Deal in December 2019, setting an EU strategy on sustainable finance and a roadmap for future work across the financial system, which is expected to be re-visited in the second half of 2020, following the public consultation of the European Commission on a renewed strategy on sustainable finance in April 2020. All these initiatives indicate significant changes of the business environment in the upcoming years.

At the same time, while the re-direction of socio-economic trends towards more sustainable paths takes place, the environmental conditions continue to deteriorate across the world, and reflection on these impacts of physical risks and environmental risks more generally in business strategies is equally important. The outbreak of the COVID-19 pandemic, with its unprecedented negative economic consequences, provides a good example that environmental hazards linked to ongoing biodiversity losses are an actual threat. From a financial perspective, more often and more severe natural disasters will be associated with bigger, potentially non-insured, losses that may rapidly threaten the solvency of households, businesses and governments, and therefore affect also the institutions.

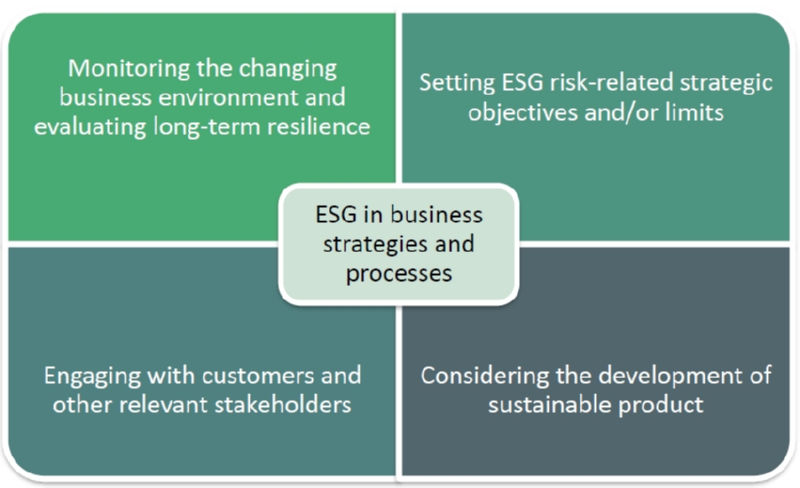

In order to reflect the ESG risks in the institutions’ business strategies and business processes, the following areas in Figure 9 were identified as the most relevant:

a. monitoring the changing business environment and evaluating long-term resilience;

b. setting ESG risk-related strategic objectives and/or limits;

c. engaging with customers and other relevant stakeholders; and

d. considering the development of sustainable products.

Expected changes in the business environment in which institutions operate are typically monitored and reflected in the institutions’ business strategies. In this context, the effect of ESG factors on the business environment can be seen as relevant for the definition of institutions’ business strategies. This implies developing an understanding and monitoring of how ESG risks can affect macro-economic conditions as well as relevant sectoral business environments, for instance, through decreases in output, changes in customer preferences or shifts in technology, and of how this could in turn have negative financial implications for the institutions.

Consequently, the assessment of the business environment would be translated into considerations on how and to what extent ESG factors may change the risks to which the financial institution is exposed with a view to adapting its business strategy accordingly (for example by scenario analysis). When doing so, the specific characteristics and risks of the financial institution’s business model needs to be taken into account. Different risks may arise depending, amongst others, on the geographical location, counterparties and the economic sectors of its exposures. For example, a financial institution lending to SMEs located on a flood-prone area would face different impacts from ESG factors than an institution in a coal-intensive region heavily involved in the funding of coal-fired power plants.

When assessing the potential impact and materiality of ESG risks and in determining the resulting implications for the business strategy, it is essential to extend the planning horizons, which usually consist of 3-5 years, and equally consider risks to the business model in the longer run. This extension could be aligned with relevant public policies such as, for example, the emission reduction targets set for 2030. ESG risks and especially climate-related and environmental risks pose the challenge of manifesting not only in the short-run to medium-run, for example, due to an abruptly announced policy measure, but also over the following decades, because the physical impact of environmental change will affect economies and societies more permanently and severely, or because previously insufficient political action forces a sudden and comprehensive transition.

From a strategic point of view, institutions with a substantial proportion of their business in non-sustainable activities may face, in addition to potential financial impacts from exposures to sectors under pressure from stricter environmental or social regulation, reputational issues affecting their customers or investors base. The same could apply for institutions with a lack of commitment to sustainability objectives.

Corporate sustainability has been sometimes linked with the long-term competitiveness of corporations. Academic research shows various elements through which the long-term competitiveness might be affected, such as short-termism leading to underperformance in the long-term, both in terms of stock market as well as accounting and/or operational performance, ultimately resulting in lower returns on investment, or in difficulties to attract and retain high-quality staff, which may potentially translate into lower productivity and efficiency and, in the end, worse operational performance.

Designing (or re-designing) business strategies in order to take into account ESG risks can be based on the institutions’ existing internal processes used for translating analysis of trends and business environment into strategic objectives and/or limits.

Institutions that want to align their portfolios define ESG risk-related strategic objectives and/or limits as part of such strategies. These are in many cases disclosed and, within some international frameworks, the path to the fulfilment of the set targets is also monitored (e.g. Principles for Responsible Banking).

ESG risks are likely to affect different regions, economic (sub-)sectors, and assets differently. In light of this, the institutions’ overall objectives and targets may need to be translated into more specific targets (or limits), including exclusion policies for certain regions, sectors or activities (e.g. specific sectors or type of counterparties due to highly polluting production).

In a similar fashion, institutions could use the Sustainable Development Goals (SDG's) to mitigate physical and transition risks, e.g., SDG 6-aligned investments in projects or firms providing sustainable water supplies, water storage, water-efficiency improvements or water treatment or SDG 11 to formulate a strategic objective on financing people’s access to safe, affordable, accessible and sustainable transport systems, notably by expanding public transport.

Strategic objectives and limits can also be formulated based on the EU Taxonomy (see Chapter 5). Institutions that wish to align more closely with the EU Taxonomy could, for example, set a target on a certain proportion of their overall credit or investment portfolios to be associated with activities that qualify as ecologically sustainable under the Taxonomy.

Another important aspect when considering the integration of ESG risks into the institution’s business processes relates to enhancing the institution’s direct and indirect engagement with borrowers, investee companies and other stakeholders. Direct engagement could comprise entering into a dialogue with the stakeholder’s management or exercising voting rights in its general meeting. Indirect engagement could happen via the publication of an institution’s ESG risk-related strategies and expectations towards stakeholders or through dialogue with industry associations.

The engagement policy should consider at least two perspectives that complement each other: First, the internal perspective, i.e. which capacities and expertise an institution needs to build up in order to understand the business models of its customers and the impact of ESG factors on them. Second, the external perspective, i.e. how an institution can interact with borrowers, investee companies and possibly other stakeholders to mitigate ESG risks for the institution that originate from such stakeholders.

While an institution may focus on sustainable activities to reduce ESG risks to its financial exposures, it can also try to address these risks by starting a dialogue with its counterparties regarding their adaptation to the transition to a more sustainable economy.

On a broader scale, institutions could consider engaging with sectoral organisations in order to promote a mutual understanding on how ESG risks may be addressed by companies in the context of a specific industry, and certainly in line with the relevant laws.

If deemed necessary, institutions could assist counterparties with the development of an action plan to gradually reduce their exposures to ESG risks and provide the necessary funding to implement the action plan.

With regard to retail clients, ESG risk-related engagement could, for example, address the energy efficiency of residential homes and the effect on the future value of the property. This could have a positive effect both on their ability to repay loans and the value of the collateral in case of default.

Where relevant, institutions could also define an engagement policy for their market exposures. This could include high level actions such as a public communication from the institution setting out which measures it expects from investee companies to mitigate ESG risks or exerting a more direct interaction with investee companies.

Where institutions hold equity investments that provide them with voting rights, they should take a strategic decision on how to use their voting rights in order to mitigate ESG risks stemming from investee companies. If the institution has adopted ESG risk-related objectives and/or limits, it seems reasonable to align the policy on the exercise of voting rights with them, considering potential limitations from the concept of “acting-in-concert”.